Public Act 123

Public Act 123 has significantly changed the Michigan tax-reversion process. The new legislation establishes a three-year tax-reversion process compared to the former six-year process. Property owners with taxes that are three years delinquent will be foreclosed and the property will be sold at public auction. For example, owners who fail to pay their 2010 property taxes may lose the property to foreclosure in March 2013.

Property owners face higher interest and fees for not paying their taxes. Taxes that are delinquent for more than one year will have a substantially higher interest rate (1.5% per month, as opposed to the current 1%), and will have a $175 forfeiture fee plus additional administrative fees added.

Tax Reversion

Tax Reversion is the process by which delinquent property taxes are collected, or in lieu of collection, the process which governs the disposition of real and tangible personal property upon which property taxes remain unpaid. On July 22, 1999 Governor Engler signed into law significant changes to the Michigan Tax-Reversion process.

Former Process

The former process had often been criticized as both cumbersome and detrimental to economic development, due to the amount of time taken to return tax-reverted property to productive use. The new legislation will greatly simplify and expedite the tax-reversion process ensuring that it produces marketable title to tax-reverted property, and permit counties to exercise significant control over the handling of tax-reverted property within their boundaries with minimal involvement by the State.

New Legislation

The new legislation establishes a three-year tax-reversion process compared to the former six-year process. Annual tax-liens sales were eliminated in favor of an annual forfeiture and judicial foreclosure process. Due process and notification procedures were significantly strengthened. In addition, changes were made to expedite the handling of abandoned tax reverted property.

As under the former process, County Treasurers will be responsible for collecting delinquent taxes and for sending notices prior to forfeiture. County Treasurers will also be responsible for the foreclosure and sale of tax-reverted property unless a county elects to “opt out” of those portions of the tax-reversion process. Non-participation by a county will require a resolution to that effect adopted by the county board of commissioners, together with the written concurrence of the County Treasurer, and of the county executive, if any, by December 1, 1999. If a county elects not to participate in the foreclosure and sale of tax-reverted property, the State will be responsible for those portions of the tax-reversion in that county.

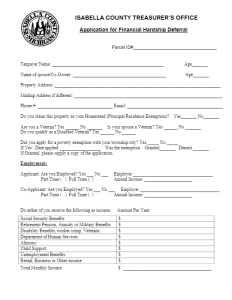

Financial Hardship Policy & Application

The Treasurer’s objective is to assist delinquent taxpayers to fulfill their Real Property Tax obligation to avoid any foreclosure on any property the property owner wants to maintain.

The Treasurer will assist any taxpayer through the year. Applications for consideration will be available at the Treasurer’s office. When site visits are conducted collectors will carry applications and distribute them when appropriate.

Financial hardship will be considered at the show cause (administrative) hearing pursuant to the prior notice. The date may also be obtained by contacting the Treasurer’s office. The Treasurer may request that an appointment be made for the orderly conduct of business. Non Appointments will be scheduled as time permits.

The applicant must establish that the property is a homestead parcel or qualified agricultural property (Pursuant to MCL 211.7dd). This may be accomplished by affidavit that they have been granted a homestead exemption that is currently in effect. Deeds or other documentation showing title and residency such as a drivers license, utility bills, voter’s registration, etc. may be requested.

Applicants must also have available at the hearing:

- State and Federal tax returns for the past two years.

- Verification of income:

- Social Security Statement

- Land Contract, Leases

- State Assistance Statements

- Financial Statement of Condition (Balance Sheet)

- Documentation of application to local unit for exemption and their determination

- Provide details of all attempts for assistance or borrowing and the result of this effort

Applicant Disclosure

An income guideline for the Treasurer consideration is the Poverty Guidelines as issued by the Federal Department of Health and Human Services.

Applicants will also have the opportunity to disclose other conditions that may effect their ability to pay their taxes. This may include but not limited to the following:

- Existence of physical/mental disabilities

- Health issues

- Outstanding financial obligations due to condition/factors outside the individual’s control

- Unemployment

Potential Assistance

It will be determined if the applicant has exhausted all potential sources of assistance. A comprehensive list will be distributed to those applying for hardship exemption which will include the following:

- Federal, State and Local governmental agencies

- Non-Profit, Charitable organizations

- Community based and service groups

Determination

A list of all applying for hardship deferrals will be forwarded to the respective local unit. The Treasurer will attempt to determine if the hardship is temporary or permanent. For temporary hardships the anticipated time to correct the situation will be determined. Permanent hardship cases will also be referred to respective local units for future relief under MCL 2117u.

The granting of a hardship waiver only extends the time to pay the delinquent amount due. Interest is 1.5% monthly and any additional expenses continue to accrue on the parcel, increasing their liability. Ultimately the Treasurer will determine if relief from foreclosure will enable the taxpayer to pay their delinquent tax within twelve months of his decision.

Hardship determination at the administrative hearing will be in the sole and absolute judgment of the Treasurer.

Hardship Application Deferral